Estate Planning Series Now Live! Educational Guides & Downloadable Resources: Explore The Series →New Civic Guide & Download: Georgia Voters: How to Check Your Registration Status Get Started →New: Homeowner Financial Guidance on Property Taxes & Homestead Exemptions Learn More →

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

This resource is a simple way to organize essential information—so your loved ones aren’t left guessing. This binder helps you gather important details in one place for emergencies, illness, or unexpected events.

Organization—not documentation overload

This binder focuses on awareness and organization. It does not ask for sensitive data or replace legal, medical, or financial documents.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

A gentle guide to starting important estate planning conversations—without pressure or perfection. These prompts help remove emotional barriers and make it easier to begin discussions at your own pace.

You don’t need the perfect words

This guide is not a script or a checklist. It’s a supportive starting point to help you open conversations when the timing feels right.

Inside this Toolkit

Conversation starters for spouses or partners

Prompts for talking with adult children

Guidance for approaching parents or older relatives

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

A clear look at estate planning risks and what can happen when decisions are delayed—and why awareness matters. This brief snapshot outlines common risks so you can understand potential consequences before a crisis forces decisions.

Progress matters—even if it’s slow

This resource is designed to inform—not overwhelm. It provides a straightforward overview so you can decide your next steps with clarity and confidence.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

Beneficiary designations play a major role in how your accounts transfer after you pass away, yet many people overlook how these designations actually work.

Beneficiary designations determine who receives certain accounts instantly when you pass away — outside probate and sometimes even outside your will or trust.

You should review your designations because:

They override the instructions in your will or trust

Many people accidentally leave ex-spouses or deceased relatives on old accounts

They ensure accounts pass smoothly to the person you intend

They keep assets out of probate

They are one of the simplest and fastest ways to protect your family

This article explains what beneficiary designations do, which accounts they affect, and how to set them correctly.

⚖️ What Beneficiary Designations Actually Do

A beneficiary designation is a legal instruction you give directly to a financial institution stating who should receive your:

Key point: Beneficiary designations bypass your will and your trust unless you intentionally name the trust itself as the beneficiary.

Bank accounts with POD/TOD instructions

Retirement accounts

Life insurance

Investment accounts

Certain brokerage accounts

Annuities

Pension or employer benefits

When you pass away, the institution transfers the asset directly to the beneficiary—no probate, no court involvement. This is where many plans quietly break.

FREE DOWNLOAD

📘 Beneficiary Check-Up Toolkit

The Beneficiary Check-Up Toolkit helps you confirm — in writing — whether your account designations actually match your intentions. View resource →

⚖️ Types of Beneficiaries

Primary Beneficiary The first person (or persons) who will receive the asset.

Contingent Beneficiary The backup — receives the asset only if the primary beneficiary cannot.

Per Stirpes Option Ensures your share passes to your beneficiary’s children if they pass away before you. This prevents accidental disinheritance.

⚖️ Accounts That Should Always Have Updated Beneficiaries Designations

Retirement Accounts 401(k)

403(b)

IRA / Roth IRA

SEP / SIMPLE IRA

Life Insurance Policies

Investment/Brokerage Accounts Many allow a Transfer on Death (TOD) designation.

Bank Accounts Many banks allow Payable on Death (POD) setup.

Employer Benefits Pensions Workplace life insurance Deferred compensation plans

HSAs (Health Savings Accounts) If no beneficiary is listed, the account may become fully taxable.

⚖️ What Happens If You Don’t Add a Beneficiary

If you leave a beneficiary blank:

The asset may go through probate

The state decides who receives it

Taxes may be higher for heirs

The wrong person may inherit (based on default laws)

There may be delays of months or even years

Worst-case scenario:

Your ex-spouse or someone you removed from your will still gets the asset if they remain named on the account. This happens more often than most people realize.

⚠️ Many families believe updating a will updates beneficiaries—it does not.

⚖️ When Your Trust Should Be the Beneficiary

There are times when naming your trust may the smarter route:

You want asset protection for beneficiaries

You want to manage distributions over time (not all at once)

You have blended family scenarios

You want centralized control under one document

You want a trustee to manage funds for minor children

But caution: Retirement accounts have special tax rules. Consult a professional before naming a trust as beneficiary.

⚖️ How Often Should You Review Beneficiary Designations?

Review them:

Every 1–2 years

After major life events: Marriage or divorce

Birth or adoption

Death of a beneficiary

New accounts opened

Major financial changes

Also confirm your full legal name and your beneficiaries’ names are correct and spelled properly. Financial institutions still use whatever is on file — even outdated or misspelled names.

⚖️ Quick Checklist You Can Use Today

Update or confirm beneficiaries on:

Savings and checking accounts (POD)

Investment accounts (TOD)

Employer retirement plans

IRAs / Roth IRAs

HSAs

Life insurance policies

Pensions

Employer-paid benefits

Annuities

Verify each account has:

A primary beneficiary

A contingent beneficiary

“Per stirpes” selected, if appropriate

Matching full legal names

Your trust listed when that is your intended instruction

This 20-minute exercise can prevent years of legal problems.

🛠️ Downloadable Resources

Start with one or two of these simple tools which are designed to help you feel informed, empowered, and ready to take meaningful next steps.

FREE DOWNLOAD

📘 Beneficiary Check-Up Toolkit

A guided worksheet to help you confirm — in writing — who is listed on each account and whether those designations match your wishes. View resource →

Looking for more estate planning tools? Explore the full collection on our Estate Planning Resources page.

➡️ Next Up: Move into Phase 2: Trusts, Strategy & Asset Protection

Now that you’ve completed Phase 1, move into Phase 2 which explains how trusts work, why families often choose them, and how to properly fund, structure, and maintain them to avoid common and expensive mistakes. This phase moves readers from basic understanding into practical, action-oriented planning.

Explore trusted, expert sources or related articles for deeper guidance on the topics covered in this phase.

📚 Trusted External Resources

These organizations provide clear, introductory guidance on estate planning concepts, documents, and decision-making. Their resource hubs are designed for broad learning and ongoing exploration.

About the Author Written by Tonya Harris, founder of Elevated Sand. Tonya creates culturally grounded financial and digital education that helps people understand complex topics and make informed decisions for the future.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

The Common Misunderstanding: Many people assume “I created a trust, so I don’t need a will anymore.” It sounds logical. Trusts are powerful tools, and they can handle a lot.

But even the best-designed trust doesn’t replace everything.

A Revocable Living Trust avoids probate, protects privacy, and distributes assets efficiently — but it is not a complete estate plan on its own.

⚖️You still need a will because:

A will handles anything not titled in your trust

A will allows you to name guardians for minor children

A will gives legal instructions for personal items and sentimental property

A will activates your pour-over clause, ensuring all remaining assets flow into the trust

A will prevents the state’s default rules from taking over

If you’ve ever wondered why attorneys still draft a will alongside a trust, you’re in the right place. This guide will show you — in simple terms — what a will still does and why both tools matter.

⚖️ What a Trust Covers (and What It Doesn’t)

A revocable living trust is powerful, but it only controls assets that are:

Correctly retitled in the trust’s name

Assigned to the trust through proper funding documents

Linked by beneficiary designations or assignment forms

If you forget to fund something… the trust can’t touch it.

Common assets people forget to place in their trust:

Vehicles

Recently purchased property

Newly opened bank accounts

Refunds, rebates, or settlement checks

Digital assets and online accounts

Personal belongings

The trust has no automatic authority over unfunded assets. A will is your safety net.

⚖️ The Pour-Over Will: Your Trust’s Backup System

Most modern estate plans include a pour-over will, which does exactly what it sounds like:

It “pours” any leftover assets into your trust after you pass away.

This protects you when:

You forgot to transfer an asset

You acquired something new shortly before death

Paperwork wasn’t completed in time

Someone else is holding the asset (a business, lender, or third party)

Without this will, those assets:

Must pass through probate

Will be distributed based on state law — not your trust’s instructions

Could end up going to the wrong person

A trust without a will is like a home without insurance — great until something goes wrong.

⚖️ What a Will Covers (and What It Doesn’t)

💡 A Will Is the Only Place to Name Guardians for Minor Children

A trust cannot:

Appoint guardians

Select who raises your children

Direct parenting decisions

Only a will gives the court binding legal guidance about:

Who you trust to raise your children

Backup guardians

Whether siblings must stay together

Any special considerations (religious, emotional, educational)

Without this:

The court chooses

Your wishes may not be known

Family disagreements can erupt

A guardian you would never choose may be appointed

A will avoids heartbreaking uncertainty.

💡 Your Will Handles Personal Property and Sentimental Items

Trusts focus on financial and titled assets. Wills traditionally handle personal belongings, such as:

Jewelry

Artwork

Family heirlooms

Collectibles

Furniture

Photos and keepsakes

A well-drafted will even allows you to attach a Personal Property Memorandum — a simple list that you can update without rewriting your will.

💡 Your Will Speaks for Everything Outside the Trust

Even with excellent trust funding, there will always be “loose ends” that a will handles:

1. Final wishes not covered in your trust

Such as:

Burial or cremation instructions

Certain ceremonial or religious requests

Family notice preferences

2. Debts, taxes, and administrative details

Your will names someone who has legal authority to:

Pay remaining bills

File final tax returns

Close accounts

Work with attorneys, accountants, and insurance companies

3. Distributions to people or charities not named in the trust

A will can leave:

Specific gifts

Charitable bequests

Instructions to individuals not handled by the trust

⚖️What Happens If You Only Have a Trust (No Will)

If you pass away with a trust but no will:

Any unfunded assets must go through probate The court must appoint someone to administer those assets — even if your trust is complete.

The state determines who receives leftover property Trust instructions do not apply to unfunded assets.

Guardianship decisions are left entirely to the court A judge will choose without your guidance.

Your family may face delays and unnecessary expenses Probate becomes longer and more complicated when no will exists.

Sentimental items may be divided poorly Without clear instructions, small items can cause big arguments.

⚖️A Trust + A Will = The Complete Plan

Think of it this way:

The Revocable Living Trust Manages and distributes your assets.

The Will Covers everything your trust doesn’t — especially guardianship and unfunded items.

Think of the trust as the engine—and the will as the seatbelt.

Together, they create:

Clarity

Coverage

Flexibility

Legal protection

Peace of mind

Neither document replaces the other.

⚖️What You Should Do Now

To build a complete plan:

Confirm all assets are properly titled in your trust

Review and update your beneficiary designations

Ensure you have a legally valid pour-over will

Name primary and backup guardians (if you have minor children)

Add or update your personal property memorandum

Revisit your plan at least every 2–3 years or after major life events

A trust does the heavy lifting — but your will fills in the gaps.

Together, these decisions form a complete foundation — preparing you to move from understanding into building your plan.

🛠️ Downloadable Resources

Start with one or two of these simple tools which are designed to help you feel informed, empowered, and ready to take meaningful next steps.

FREE DOWNLOAD

📘 Will & Trust Comparison Guide

A clear, side-by-side snapshot showing when a will is enough — and when a trust adds the protection your family needs. View resource →

Looking for more estate planning tools? Explore the full collection on our Estate Planning Resources page.

➡️Next Up: Understanding Beneficiary Designations

This article explains what beneficiary designations do, which accounts they affect, and how to set them correctly.

Explore trusted, expert sources or related articles for deeper guidance on the topics covered in this phase.

📚 Trusted External Resources

These organizations provide clear, introductory guidance on estate planning concepts, documents, and decision-making. Their resource hubs are designed for broad learning and ongoing exploration.

About the Author Written by Tonya Harris, founder of Elevated Sand. Tonya creates culturally grounded financial and digital education that helps people understand complex topics and make informed decisions for the future.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

⚖️ Introduction: Consequences of Avoiding an Estate Plan

Many people assume that “doing nothing” means simply putting off a will or trust for another day. But the truth is far more serious. When no plan is in place — no will, no trust, no powers of attorney — the law steps in to make decisions for you. And those decisions rarely reflect what you would have wanted.

Doing nothing creates two categories of risk:

The risk if you become incapacitated while you’re still alive, and

If you die without a will or trust (intestacy).

⚖️ Doing Nothing – Quick Highlights

Here’s what happens when you do nothing — and why it creates stress, delays, and court involvement for your family:

You lose control during incapacity. Without powers of attorney, your family must go through guardianship or conservatorship to manage finances and medical care.

The court chooses your decision-makers. A judge, not you, selects who will handle your money, bills, and health decisions.

Probate becomes mandatory. If you die without a will or trust, your estate must go through a public court process.

State laws decide who inherits. Your true wishes may not be followed — especially for blended families, unmarried partners, or estranged relatives.

Minor children face added risk. The court chooses guardians and controls their inheritance.

Family conflict becomes more likely. When no plan exists, emotions, assumptions, and disagreements escalate.

These situations affect families in dramatically different ways, but both share one painful theme: your loved ones lose control at the very moment they need clarity and stability the most.

This article walks you through both scenarios, how they unfold in real life, and what families can expect if no estate plan is in place.

⚖️ What Happens If You Become Incapacitated

Most people think that estate planning is only about death, however, the first legal crisis usually happens while someone is still very much alive.

A sudden illness, a stroke, surgery complications, dementia, or a serious accident can instantly change your ability to make decisions. When this happens — and no one has been legally appointed to act for you — your family cannot automatically step in, even if they’re your spouse or adult child. Instead, they must go to court.

If you haven’t chosen who will speak for you, then the court will.

💡 Without a Durable Financial Power of Attorney or a Medical Power of Attorney

Your family must request:

Guardianship (medical and personal decisions), and

Conservatorship (financial decisions).

Both processes involve lawyers, court hearings, medical evaluations, and ongoing court supervision. Families often describe it as one of the most painful experiences of their lives because:

They are already dealing with an emotional crisis.

Court costs can drain savings quickly.

Decisions may be delayed for weeks or months.

The judge chooses the decision-maker — not you. And sometimes the judge selects someone you would never have chosen.

This is why incapacity planning often becomes the first legal crisis families face.

💡 Your accounts may be frozen until the court steps in.

Banks and financial institutions cannot allow someone else to access your accounts, pay your bills, or manage your investments unless legal authority is properly documented.

That means:

Mortgage payments can be missed.

Utilities may be shut off.

Medical bills pile up.

Business owners may see operations stall.

In this situation, your family becomes stuck in a financial pause button at the worst possible time.

💡 Your medical care may be delayed or decided by someone you did not choose.

Doctors need to know who has legal authority to approve treatment. Without a named agent, decisions can be delayed — and in emergency situations, delay has consequences.

Families often disagree about what you “would have wanted,” resulting in conflict during an already stressful moment.

📘 Want to see this laid out clearly?

FREE DOWNLOAD

The Estate Planning Risk Snapshot shows what typically happens when no plan is in place — including delays, costs, and court decisions families don’t expect.

⚖️ What Happens If You Pass Away (Intestacy)

Once someone passes away, a completely different legal system takes over. This is called intestacy — the state’s default estate plan.

When there is no will or trust, the law dictates:

Who inherits

In what order do they inherit

How much they receive

What individual(s) becomes guardian of minor children

Which party(s) serves as executor or personal representative

A primary concern is that it rarely matches what the person would have wanted.

💡 Your family must go through probate — often a long and public process.

Probate is required to:

Prove how assets should be distributed

Identify heirs

Pay debts and taxes

Transfer ownership

Without a will, the process takes longer because the court has to make more decisions. Probate is also public.

Because of this, anyone can access the file, including:

Asset lists

Debts

Family disputes

Who inherits what

For many families, this exposure feels intrusive and uncomfortable.

💡 The state, not your wishes, determines who receives your property.

Intestacy laws vary by state, but a common pattern is:

Spouse and children split the estate

If no spouse or children → parents inherit

Siblings inherit → if no parents And so on…

This can lead to outcomes you never intended:

A separated (but not divorced) spouse inherits everything

Children receive unequal or unexpected shares

Minor children inherit money outright, causing court-supervised accounts

Stepchildren are completely excluded

An estranged family member becomes entitled to assets

These rules apply even if your partner, caregiver, or loved ones depend on you.

💡 Parents of minor children face the greatest risk.

If both parents pass without naming a guardian:

The court chooses who raises the children

Family members may disagree

Children may be temporarily placed with someone they don’t know

Financial management is handled by a court-appointed conservator

Most parents who “meant to make a plan” regret not doing this sooner once they learn how guardianship works.

💡 Your loved ones may lose time, money, and emotional peace.

Doing nothing can create:

Delays in receiving assets

Family conflict or resentment

Legal fees that reduce inheritance

Confusion about your true wishes

Hardship for surviving spouses and partners

Stress for adult children trying to “guess” what you wanted

Families often say the same thing afterward: “We wish they had left clear instructions.”

⚖️Change “Doing Nothing” into “Getting Started”

Doing nothing doesn’t preserve the status quo — it hands control over your life and legacy to the court system. Whether through incapacity or intestacy, your loved ones are left with:

Uncertainty

Delays

Added costs

Emotional strain

Legal oversight they never expected

With a few essential documents — a will, trust (when appropriate), and financial and medical powers of attorney — nearly all of these problems can be avoided.

Giving your clarity.

Providing direction.

Creating peace of mind.

And that is the true purpose of estate planning.

This is why even simple planning steps matter — and why details like beneficiary designations can quietly undo good intentions if overlooked.

🛠️ Downloadable Resources

Start with one or two of these simple tools which are designed to help you feel informed, empowered, and ready to take meaningful next steps.

📘 Starter Estate Planning Checklist

FREE DOWNLOAD

A simple list of decisions and documents to help you begin building a basic plan. View resource →

📘 Estate Planning Risk Snapshot

FREE DOWNLOAD

A one-page summary that shows exactly what happens when no documents are in place — court process, costs, delays, and state decisions. View resource →

Looking for more estate planning tools? Explore the full collection on our Estate Planning Resources page.

➡️Next Up: Why You Still Need a Will (Even with a Trust)

This article explains why a will remains essential, even if a trust is in place. It clarifies responsibilities that trusts cannot cover, including guardianship, personal property, and the “pour-over” function that keeps everything coordinated.

Explore trusted, expert sources or related articles for deeper guidance on the topics covered in this phase.

📚 Trusted External Resources

These organizations provide clear, introductory guidance on estate planning concepts, documents, and decision-making. Their resource hubs are designed for broad learning and ongoing exploration.

About the Author Written by Tonya Harris, founder of Elevated Sand. Tonya creates culturally grounded financial and digital education that helps people understand complex topics and make informed decisions for the future.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

Estate planning can feel confusing because there isn’t one “right” answer. The right tools depend on:

your family situation,

your goals,

what you own, and

how you want things handled.

The good news: you don’t need a law degree to understand the basics. By the end of this guide, you’ll know exactly what each tool does — and which one fits where.

⚖️ Do I Need a Will, a Trust, or Both?

Why This Question Matters

When it comes to wills and trusts, many people believe they must choose between a will or a trust. In reality, most families need both. Each serves a different purpose, and together they create a complete plan that:

Immediate protection for you while you’re alive

Protects your loved ones after you’re gone

Keeps your wishes clear and legally enforceable

Therefore, understanding differences between wills and trusts helps you avoid gaps, delays, and expensive court involvement.

⚖️ What is a Will?

A will is a written document that takes effect only after you pass away.

💡Benefits of a Will:

A will is the legal document that speaks for you after you pass away. It allows you to clearly state who should receive your property, who should handle your estate, and—most importantly for parents—who should raise your minor children. Without a will, these decisions are made by the court based on state law, not personal preference.

A will also serves as a safety net for anything that falls outside your trust. Assets that were never transferred, recently acquired property, or personal items that were not formally titled still need clear instructions. In addition, a will is the only place where you can legally name guardians for your children and provide guidance on personal belongings, sentimental items, and final wishes.

However, a will does not avoid probate, does not control assets with beneficiary designations, and does not provide protection or decision-making authority while you are alive. It plays a critical role—but it is only one part of a complete estate plan.

💡Limitations of a Will

A will does not:

A will does not avoid probate.

Doesn’t control assets with beneficiary designations.

Cannot guide financial or medical decisions while you’re alive.

It also does not provide ongoing oversight for minors or vulnerable beneficiaries.

Example: If you have a will that leaves your home to your daughter, the court must still validate the will before she can take legal ownership.

Even if you have a trust, you still need a will—specifically a pour-over will—to ensure everything is properly transferred.

⚖️ What is a Trust

A trust is a legal document governing asset transfer, before or after death, to an account managed by yourself or others.

The three main types of trusts are revocable, irrevocable, and testamentary.

Revocable trust can be changed during the creator’s lifetime

Irrevocable trust cannot be changed once established

Testamentary trust is created through a will and only takes effect after the creator’s death

Note: The series focuses on Revocable Living Trusts unless otherwise stated:

A revocable trust (or living trust) is a legal document created during your lifetime to hold and manage your assets, allowing you to control them, avoid the public probate court process, and seamlessly transfer them to beneficiaries after death, all while retaining the power to change or cancel the trust anytime.

💡Benefits of a Revocable living trust

Trusts provide capabilities a will does NOT offer:

A trust works both during your lifetime and after your passing. When properly set up and funded, it allows your assets to be managed privately, avoids the probate court process, and provides clear instructions for how and when assets should be distributed to beneficiaries.

One of the most important benefits of a revocable living trust is continuity. If you become incapacitated, the successor trustee can step in immediately to manage trust assets without court involvement. This prevents financial disruption and ensures bills, property, and investments are handled smoothly.

Trusts are also especially useful for families who want greater control. They allow you to set conditions around distributions, protect minors or vulnerable beneficiaries, address blended family concerns, and maintain privacy. While a trust offers flexibility and efficiency, it only governs assets that are properly titled or assigned to it—meaning it must work alongside a will to fully protect your plan.

Because the trust is “revocable,” you can:

You remain in control (you can change or revoke it anytime).

Add or remove assets

Update beneficiaries

Replace your trustee

⚖️ Wills vs. Trusts — How They Work Together

For many families, the real confusion starts when they assume choosing one tool means giving up the other.

Feature

Will

Trust

When it takes effect

After death

During life and after death

Avoids probate

❌ No

✅ Yes (if properly funded)

Works during incapacity

❌ No

✅ Yes

Controls timing of distributions

❌ Limited

✅ Yes

Names guardians for minor children

✅ Yes

❌ No

Provides privacy

❌ Public court process

✅ Private

Covers personal belongings

✅ Yes

❌ No

Governs untitled or forgotten assets

✅ Yes (after probate)

❌ No

Manages assets across states

❌ No

✅ Yes

Helpful for blended families

⚠️ Limited

✅ Strong

Requires proper setup to work

⚠️ Simple

⚠️ Must be funded

📌 Most families do not choose between a will or a trust — they use both to avoid gaps, delays, and court involvement.

⚖️When a Will Alone Is Enough

A will may be sufficient if you:

Own very few assets

Rent and do not own real estate

Do not mind your estate going through probate

Have an extremely simple family situation

Don’t have minor children or caregiving responsibilities

Even then, you still need medical and financial powers of attorney.

⚖️When You Absolutely Need a Trust

A trust is strongly recommended if you:

Own a home

Have minor children

Want to avoid probate

Have family members with disabilities

Own property in multiple states

Are in a blended family

Want to maintain privacy

Hold investments or significant savings

Want to protect your children from receiving lump sums

Most families fall into one or more of these categories.

⚖️Wills and Trusts: Why Most People Need Both

Think of a will and trust as teammates:

The will names guardians and covers anything left outside the trust.

The trust holds and manages major assets smoothly and privately.

Together they ensure no gaps, no court confusion, and no surprises for your loved ones.

⚖️Simple Scenarios to Guide You

Scenario

Guidance

Scenario 1: Parents with Minor Children

✔ Need a will for guardianship ✔ Need a trust for asset management ✔ Need powers of attorney for incapacity

Scenario 2: A Homeowner in a Simple Family

✔ A trust avoids probate ✔ A will covers personal items

Scenario 3: Blended Family

✔ Trust ensures intentional distribution ✔ Will ensures clarity and reduces conflict

Scenario 4: Single Adult with Only Bank Accounts

✔ Will may be sufficient ✔ Powers of attorney still essential

⚖️Common Mistakes to Avoid

Thinking a will avoids probate — it does not

Creating a trust but failing to fund it

Assuming your family knows your wishes

Forgetting to update beneficiary forms

Believing trusts are “only for the wealthy”

Unfortunately, these misunderstandings lead to avoidable court delays and family conflict.

📘 Not sure which direction fits your situation?

FREE DOWNLOAD

The Will & Trust Comparison Guide walks through common scenarios to help you see when a will is enough — and when a trust adds meaningful protection.

⚖️Where to Start

Estate planning isn’t one-size-fits-all. Use the list below as a quick start.

List all your major assets.

Decide who you want to manage your affairs if you’re unable.

Choose guardians for minor children.

Consult an estate planning attorney to draft documents.

Check your existing accounts to ensure beneficiary designations are up to date — that simple step alone can prevent major legal issues later

Review everything every 2–3 years.

Once you understand how these tools fit together, the real risk becomes clearer — what happens when none of them are in place.

🛠️ Downloadable Resources

Start with one or two of these simple tools which are designed to help you feel informed, empowered, and ready to take meaningful next steps.

📘 Will & Trust Comparison Guide

FREE DOWNLOAD

A clear, side-by-side snapshot showing when a will is enough — and when a trust adds the protection your family needs. View resource →

📘 Starter Estate Planning Checklist

FREE DOWNLOAD

A simple list of decisions and documents to help you begin building a basic plan. View resource →

Looking for more estate planning tools? Explore the full collection on our Estate Planning Resources page.

➡️ Next Up: What Happens If You Do Nothing

The next article explains what actually happens under state law when someone dies or becomes incapacitated without an estate plan—and why relying on “default rules” often leads to stress, delays, and conflict.

Explore trusted, expert sources or related articles for deeper guidance on the topics covered in this phase.

📚 Trusted External Resources

These organizations provide clear, introductory guidance on estate planning concepts, documents, and decision-making. Their resource hubs are designed for broad learning and ongoing exploration.

About the Author Written by Tonya Harris, founder of Elevated Sand. Tonya creates culturally grounded financial and digital education that helps people understand complex topics and make informed decisions for the future.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.

Estate planning isn’t just about documents and signatures. Rather, it’s about peace of mind. It’s a proactive step that ensures your family, property, and wishes are protected when life takes an unexpected turn.

Many people delay estate planning because it feels complicated, unnecessary, or reserved for the wealthy. Whether you own a home, care for loved ones, or simply want your affairs in order, estate planning gives you control over what happens next.

As families grow more diverse and financial lives expand across digital and physical assets, planning ahead has never been more essential. Clear decisions today can help your loved ones avoid costly court processes, emotional stress, and uncertainty later.

This introductory article will help you understand estate planning basics – the purpose and the power. Our goal is to establish a strong foundation before diving deeper into specific topics like wills, trusts, guardianship, and protecting digital assets in the articles ahead.

⚖️ What Estate Planning Really Means

At its core, estate planning is the process of organizing your affairs so that your wishes are carried out smoothly—both during your lifetime and afterward.

Not only is It not just about who inherits your property; it’s also about making sure the right people have the right information at the right time.

It applies to anyone who has:

Children;

Property;

Bank accounts or investments;

Desires to avoid legal complications for their family; and

Wants to stay in control of medical or financial decisions.

A well-designed estate plan ensures:

Your family’s financial stability is protected;

Taxes and court costs are minimized;

The right people handle your affairs if you cannot;

Assets transfer smoothly;

Privacy and peace of mind are preserved;

Legacy is preserved according to your wishes.

Each family’s plan will look different, however, the foundation is the same: preparation and intention.

⚖️ Why Every Family Needs an Estate Plan

Families today are more complex than ever. For instance, blended households, aging parents, multi-state property, digital assets, caregiving demands, and rising healthcare costs.

That complexity makes estate planning essential. For that reason, a well-structured plan:

Minimizes family conflict – Clear instructions reduce confusion and prevent disputes during already difficult moments.

Keeps decisions out of court – When no plan exists, courts determine who controls finances and guardianship. Planning ensures your voice remains in charge.

Safeguards children and dependents – Guardianship decisions should be intentional — never left to uncertainty.

Eases emotional and financial strain – Clarity provides peace of mind for the people you love most.

📘 Starter Estate Planning Checklist

FREE DOWNLOAD

Feeling overwhelmed? Start small. The Starter Estate Planning Checklist helps you see what you already have in place and what actually needs attention. View resource →

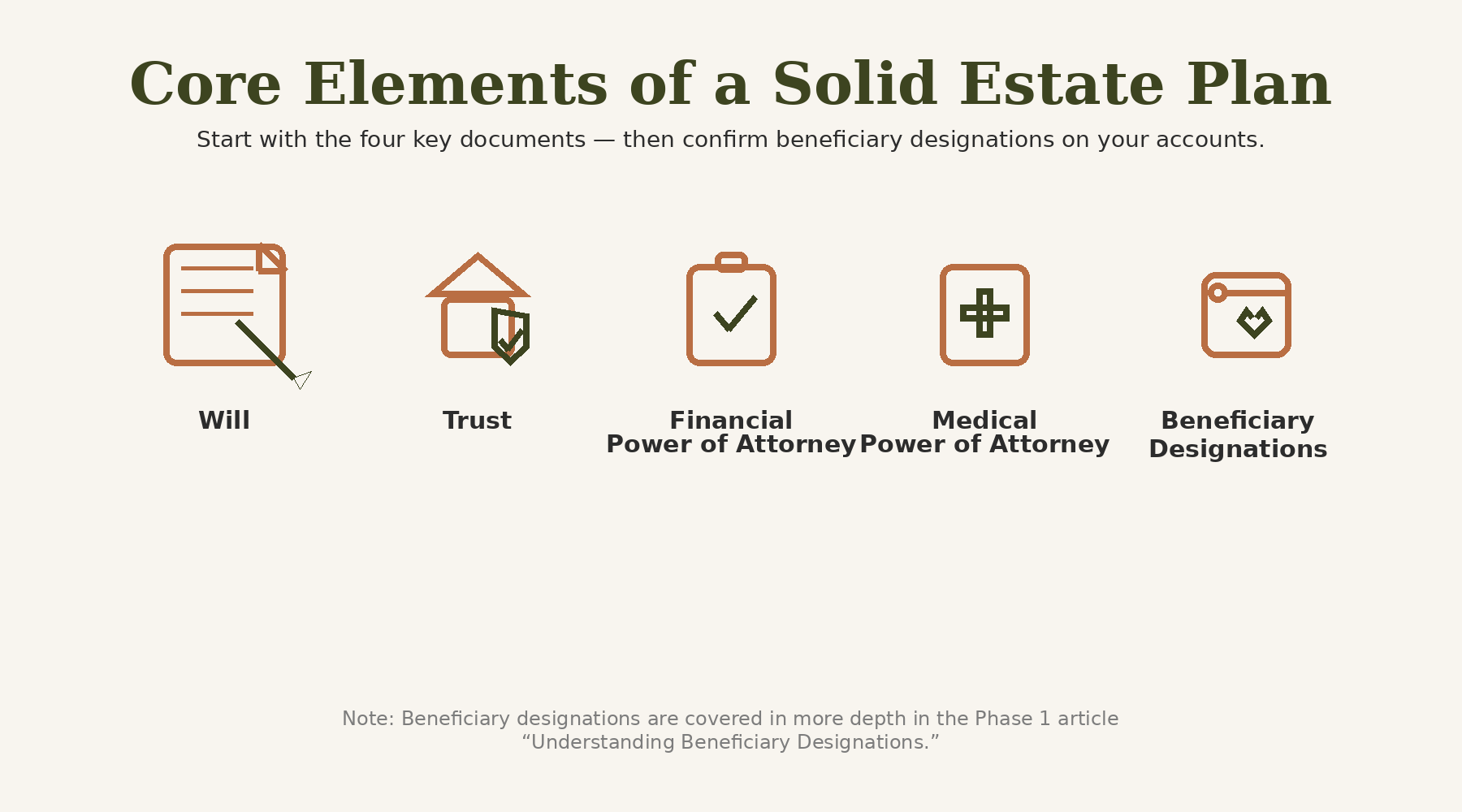

⚖️ The Core Elements of a Solid Estate Plan

Most families benefit from having these foundational documents:

Wills state who receives your property, serves as guardian for minor children, and manages your estate after your passing. Without a will, state law decides these things — not you.

Revocable Living Trusts allow you to avoid probate, keep your affairs private, transfer property in an organized, tax-efficient way, plan for disability, and maintain control over how and when assets are used. These are key examples of why trusts are especially helpful for blended families, homeowners, and anyone wanting a smooth transition of assets.

Financial Power of Attorney authorizes someone you trust to pay bills, manage accounts, handle insurance or tax matters, and oversee daily financial needs. It’s essential if you’re ever injured, ill, or unable to act.

Medical Power of Attorney + Advance Directive outlines who speaks for you during medical emergencies, your wishes for treatment and end-of-life care, and how doctors should proceed if you are unable to choose. Therefore, this person relieves your loved ones of emotional burden during difficult moments.

Together, these documents work as a system—not standalone pieces.

⚖️ What Happens Without a Plan

If you die or become incapacitated without documents in place, several issues can arise:

Probate Court Delays – Assets may be tied up for months — even years — before they are released possibly incurring attorney fees and court costs.

Higher Legal Costs – The process becomes more expensive for your family.

Family Disputes – Loved ones may disagree about your wishes, who should manage things, and who should receive what

Court-Appointed Guardians – A judge may assign guardianship for your children or appoint someone to manage your finances.

However, all of this is avoidable with proper planning.

⚖️ Key Misconceptions About Estate Planning

Let’s clear up four common misunderstandings:

I don’t have enough money to justify planning. – Estate planning is about control, not net worth.

My family knows what to do — we’ve talked about it. – Verbal conversations are not legally enforceable.

I’m too young to worry about this. – Incapacity can happen at any age. Therefore, planning early is protection, not pessimism.

A will is all I need. – A will alone does not avoid probate and does not cover medical or financial decisions during life.

⚖️ Where to Start (Simple First Steps)

You don’t need to overhaul everything at once. Begin with these manageable actions:

List your key assets (home, bank accounts, retirement accounts, life insurance).

Choose people you trust for medical and financial decision-making.

Decide who should inherit specific items or responsibilities.

Talk to a qualified estate planning attorney to formalize your documents.

Review everything every 2–3 years or after major life changes.

Now that we’ve established a foundation, the next step is understanding the two core tools (Wills and Trusts) which most families rely on — and how they actually work together.

🛠️ Downloadable Resources

Start with one or two of these simple tools which are designed to help you feel informed, empowered, and ready to take meaningful next steps.

📘 Starter Estate Planning Checklist

FREE DOWNLOAD

A simple list of decisions and documents to help you begin building a basic plan. View resource →

📘 Estate Planning Risk Snapshot

FREE DOWNLOAD

A one-page summary that shows exactly what happens when no documents are in place — court process, costs, delays, and state decisions. View resource →

📘 Estate Planning Glossary

FREE DOWNLOAD

A growing reference of essential estate planning terms to support your learning across the entire series. View resource →

Looking for more estate planning tools? Explore the full collection on our Estate Planning Resources page.

➡️ Next Up: Do I Need a Will, a Trust, or Both?

The next article walks you through the major differences, why most families actually need both, and how each document fits into your long-term plan.

Explore trusted, expert sources or related articles for deeper guidance on the topics covered in this phase.

📚 Trusted External Resources

Organizations listed below provide clear, introductory guidance on estate planning concepts, documents, and decision-making. Their resource hubs are designed for broad learning and ongoing exploration.

About the Author Written by Tonya Harris, founder of Elevated Sand. Tonya creates culturally grounded financial and digital education that helps people understand complex topics and make informed decisions for the future.

Disclaimer: Information is for educational purposes only and should not be considered legal or financial advice. Estate planning involves complex legal and tax considerations. You should consult a qualified estate planning attorney to determine the best approach for your situation and ensure compliance with your state’s laws.